For many households, the dream of homeownership has remained elusive because saving for a down payment is financially unrealistic.

As lenders tightened their underwriting standards, following the housing bust over the last decade, most homebuyers have been required to put a minimum of 3.5% to 5% down in order to purchase a home. However, a new grant program is changing the game.

Mortgage Trust, Inc. (NMLS #3250), which Swanson Home Loans is a subsidiary of, is proud to announce that we have become a participating lender for the NHF Platinum™ homebuyer assistance program.

What does this mean for you? Through this program, Mortgage Trust can help eligible families and individuals obtain a grant for a down payment and/or closing costs—a grant that does not need to be repaid.

The National Homebuyers Fund® (NHF) is a nonprofit public benefit corporation that supports affordable, responsible homeownership. NHF manages several Down Payment Assistance (DPA) programs that help people purchase a home with fewer out-of-pocket costs. DPA programs follow standard mortgage loan underwriting guidelines to ensure that borrowers are able to afford their mortgage.

The NHF Platinum™ program is designed to provide down payment assistance on the purchase of a primary residence in various states, including Oregon, Washington, and Idaho.

NHF Platinum™ Program Highlights

- Non-repayable grant, up to 5% of Loan*

- No first-time homebuyer requirement

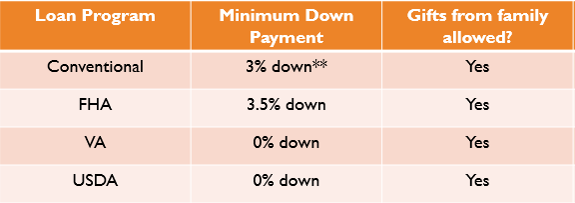

- Conventional, FHA, VA and USDA Mortgages

- FICO scores as low as 640

*Certain restrictions apply on all programs. Contact Evan Swanson NMLS 120856 to learn more about Borrower Eligibility, Rates, Terms, and Guidelines.