St. Patrick’s Day is this coming Sunday which may have you thinking if you should look at borrowing money from a leprechaun instead of your favorite mortgage lender? Well, you can but last time I checked leprechaun’s are always coming up short……

Mortgage Rates

Home Loan interest rates remain at 10-month lows. Might they go even lower? Some of the current economic headlines are interest rate friendly.

Jobs Report

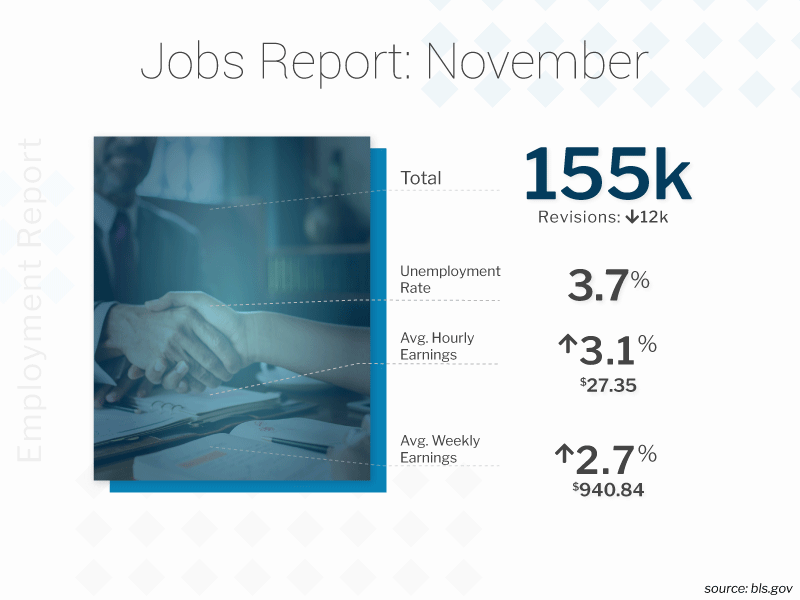

As I wrote in last week’s post I was very keen on seeing the results of Friday’s all-important employment report. Initially when I saw the unemployment rate drop from 4.0% to 3.8% I was concerned that mortgage rates may rise (good news for the economy tends to be bad news for rates).

However, according to the report only 20,000 jobs were added to the US economy in February and analysts had been expecting +170,000.

Overall the results were disappointing which is favorable for mortgage rates.

Inflation Data

Earlier today the Labor Department released the Consumer Price Index (CPI). Year-over-year prices increased by the slowest clip in over two years (+1.5%). If you strip out volatile food & energy prices the core CPI increased by 2.1%. These are considered “tame” price increases which is good for mortgage rates.

Outlook

The remainder of this week’s economic calendar is relatively light. The highlights include the Producer Price Index and Durable Goods on Wednesday followed by New Home Sales and Consumer Sentiment on Friday.

I recommend maintaining a floating position.

Current Outlook: floating